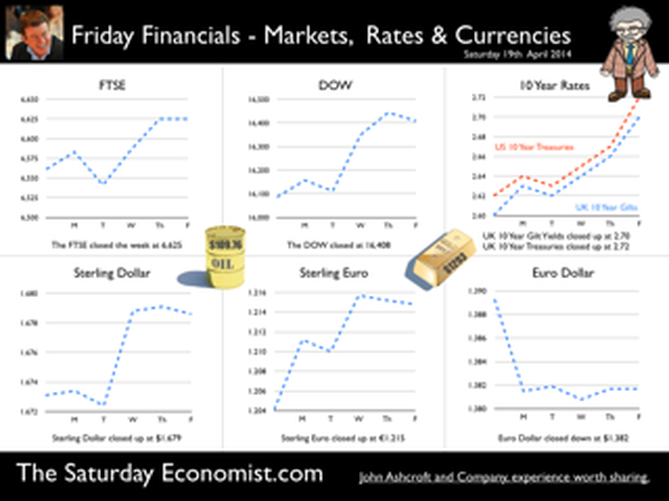

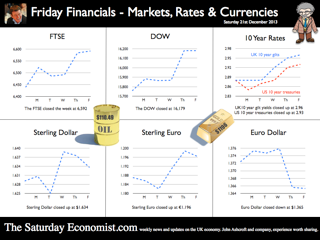

Janet Yellen was speaking at the Economic Club of New York this week. Three big questions continue to dominate policy formulation at the Federal Reserve. Unemployment, inflation and factors which may push the recovery off track. Actually, that’s more than three but … According to the Fed forecasts, US unemployment is set to fall to around 5.5% by the end of 2016 and inflation will hover just below 2%. “The economy would be approaching maximum employment and price stability for the first time in nearly a decade”. That's NICE! And what of interest rates? “Economic conditions, may for some time warrant keeping short term interest rates below levels the Committee views as likely to prove normal in the longer run”. The markets reacted well. The Dow moved up and the dollar moved down. Sterling moved to $1.679. In March, the Fed chair had given a clear indication that rates would start to rise in the first quarter of 2015. Less than a month later, there was no such clarity. Rates will be on hold until the recovery is well established. As long as it takes. Unemployment rate, the measure of momentum that really matters, to the doves at the Fed. Exogenous Shocks Nowhere in the speech did the “Capsid Bug” feature. According to a report in The Times today, black pod disease and capsid bug infestations are ravaging cocoa crops in West Africa. This shock to supply plus the surging demand from Chinese Chocaholics is causing a cocoa pop. Cocoa beans have jumped in price from $2,680 per tonne in January to over $3,000 per tonne in March. There could be a 115,000 tonne shortfall in supply this year. By next Easter, we may well be eating smaller eggs which cost much more. So much for the threat of world deflation! Does this matter? Well yes. The collapse of the Peruvian anchovy crop in 1972/3 was claimed by many to herald the onset of the hyper inflationary episode of the seventies. OK, the Russian grain famine, the onset of OPEC and the quadrupling of oil prices assisted considerably. But the message is, exogenous shocks from commodity prices can have a greater impact on domestic inflation. Much greater than the Phillips curve paradigm, much beloved by the FOMC, provides. This is clearly demonstrated in the UK economics data released this week. Inflation is falling, employment is rising. World prices mitigated by the appreciation of Sterling are marking the price changes. UK Inflation Inflation CPI basis slowed to 1.6% in March from 1.7% in the prior month. Goods inflation fell to 1.0% and service sector inflation fell to 2.3% (2.4%). Oil related transport costs were dominant in the slow down. Manufacturing output prices increased by just 0.5% as input costs actually fell by 6.5%. The fall in crude oil prices, imported metals, parts and equipment largely explained the fall. Sterling appreciation assisted the process. Sterling averaged $1.66 in March this year compared to $1.51 last year. A 10% appreciation assisting the “deflationary process” significantly. [Oil prices Brent crude basis averaged $108 approximately in both months]. So what of employment? Unemployment figures - Jobcentres will be closing by the end of 2016 Unemployment fell to 6.9% in the three months to February to a level of 2.24 million. This is below the level originally outlined in the Bank of England Forward Guidance in August last year. 7.0% the level at which the Bank would begin to consider an increase in base rates. The claimant count fell by 30,000 to a level of 1.142 million. Over the last three months, the count has fallen by 100,000 and almost 400,000 over the last twelve months. If current rates persist, the labour market will fall to pre recession levels towards the end of the year. By the end of 2016, No one will be left on the list. So this is what they mean by full employment! Jobcentres will have to close! The implications for earnings are evident. Already in February, whole economy earnings increased by 1.9% and wages in manufacturing and construction increased by 3%. We expect a significant acceleration in earnings throughout the year as the labour market tightens considerably. As for base rates, Yellen is signalling the US rates will be kept on hold well into 2015. The Bank of England may well have no such luxury. The MPC will be reluctant to raise rates ahead of the Fed. If this were to happen, despite the inherent structural weakness on trade and the current account, sterling will continue to rise significantly. $1.73 the next target? So what happened to sterling this week? The pound closed at $1.679 from $1.673 and at 1.215 from 1.204 against the Euro. The dollar closed at 1.382 from 1.3389 against the euro and at 102.42 against the Yen. Oil Price Brent Crude closed at $109.76 from $107.70. The average price in April last year was $101.2. The energy kicker to falling prices may well be over. Markets, the Dow closed up at 16,408 from 16,086and the FTSE also closed up at 6,625 from 6,561. UK Ten year gilt yields closed at 2.70 (2.60) and US Treasury yields closed at 2.72 from 2.62. Gold moved lower to $1,293 from $1,318. The pattern is bullish for equities.. That’s all for this week. Join the mailing list for The Saturday Economist or forward to a friend. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

0 Comments

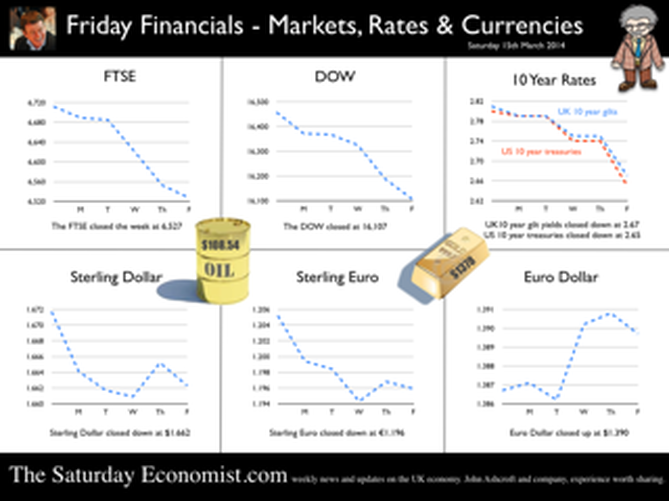

UK march of the makers … Good news for the march of the makers this week, - manufacturing output increased by 3.3% in January compared to disappointing growth of just 1.9% in the final quarter of 2013. Still some way to go to restore the sector to positive growth. Output remains some 9% below the peak registered in the first quarter of 2008. Output of Investment and capital goods increased by 3.8%, continuing the strong trend since the setback in 2008. We expect manufacturing output to increase by 2.9% for the year as whole and around 2.7% in the following year. Consumer goods output remained weak with further declines in the month. For some sectors of manufacturing, the march of the makers is more like a retreat from Moscow, than a move across the Rhineland. The makers will fail to make a real contribution to the rebalancing agenda. So what of net trade … The trade figures for January were released this week. After the December aberration, a month in which the ONS appears to have lost some £2 billion of imports, the total trade balance returned to normality. A deficit of £2.6 billion compared to £0.7 billion last month. There was a trade shortfall of £9.8 billion on goods, partly offset by an estimated surplus of £7.2 billion on services. For the year as a whole, we expect the trade deficit in goods to increase to £114 billion, offset by a trade in service surplus of £85 billion. The overall trade in goods and services shortfall will be £29 billion. At less than 2% of GDP, the deficit will not pose a threat to the outlook for sterling, assuming investment capital flows recover. The trade deficit will fail to make a real contribution to the rebalancing agenda. And what of Construction … Good news in construction. Output increased by 5.4% in January compared to the same month last year. New work increased by almost 6% in the month, as repair and maintenance budgets also increased by 4.5%. For the year as a whole we expect construction growth of around 6%, with strong growth in housing and commercial property expansion fuelling growth. Prospects for the year … The OECD suggests the UK economy will grow by over 3% in the first half of the year, in line with the strong expectations from the Bank of England “Nowcasting” model, news of which was also released this week. The NIESR GDP tracker for February suggests growth may have slowed to 2.6% in February after strong growth of 3.2% in the prior month. For the year as a whole most forecasters are moving to a 2.7% growth figure. Seems reasonable for now. The recovery appears secure and sustainable. Growth up, unemployment down, inflation down and borrowing heading in the right direction. Just the trade figures will continue to disappoint as we have long pointed out. Charlie Bean on the North East Scene … Charlie Bean was in the North East this week, delivering a speech to the Chamber of Commerce. Further reassurance the MPC will be doing its utmost to ensure that recovery is not nipped in the bud. “When the time does come for us to start raising Bank Rate, we should celebrate that as a welcome sign that the economy is finally well on the road back to normality”. Excellent. Much of the rest of the speech was devoted to investment, productivity and net trade. As the deputy governor points out, the United Kingdom has run a persistent trade deficit of the order of 2-3% of GDP since the beginning of the century. So much for “rebalancing”. On investment, productivity, depreciation and “on shoring”, the speech demonstrates the lack of fundamental understanding of the real economy amongst policy makers at a senior level. We had hoped for better from the new regime. Charlie represents the old guard due to retire in June this year. Of The Treasury Select Committee … The Governor and members of the MPC were in front of the Treasury Select Committee this week. The protocol still eludes the new man. Governor Carney actually winked at Chairman Tyrie at one stage. It is difficult to imagine Governor King, managing a nod let alone a wink. It appears the meetings of the MPC are minuted and recorded. Then for good measure the tapes are destroyed. Lack of good recording equipment formed part of the explanation by the old guard. The solution to invest in better equipment seemed a little too obvious for the Chairman and the new Governor. Expect a rethink! Wink Wink. So what happened to sterling? The pound closed at $1.662 from $1.672 and at 1.196 from 1.205 from against the Euro. The dollar closed at 1.390 from 1.387 against the euro and 101.31 from 103.3 against the Yen. Oil Price Brent Crude closed at $108.34 from $108.86. The average price in March last year was $108. Markets, moved down concerned about China and the Ukraine - The Dow closed at 16,107 from 16,458 and the FTSE closed at 6,527 from 6,712. UK Ten year gilt yields closed at 2.67 from 2.81and US Treasury yields closed at 2.65 from 2.80. Gold loves a crisis, closing up at $1,378 from $1,338. That’s all for this week. No Sunday Times and Croissants tomorrow. All records of the tennis results will be recorded then destroyed. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

UK rates on hold …

No surprise this week - the MPC voted to keep rates on hold and maintain the size of the asset purchase programme at £375 billion. It will be some months yet before rates begin to rise. Our current assumption is that rates will begin to rise in the second quarter of 2015. 40% of respondents in the latest Bank of England/GfK Inflation survey expect rates to rise over the next twelve months. No worries for the future apparently. Once on the rise, over 70% expect rates to be less than 3% in five years time. So much for the madness of crowds. Clearly the general public have a much better grasp of the latest simulations of the “equilibrium real interest rate associated with a neutral monetary policy over the medium term” than is generally assumed. They must have been listening to the speech by David Miles last month. Asked about the current rate of inflation, the median answer was 3.5% down from 4.4% in November. Excellent. So much for the madness and the wisdom of crowds. US Payroll data up … In the USA, better than expected payroll data guarantees the Federal Reserve will continue to taper, with a further reduction this month to $55 billion. Employers added 175,000 more jobs in February. Movement in US futures suggest the markets attach a "higher probability to a US rate rise in the middle of 2015". Fed officials have said they are “comfortable with market expectations of future rate rises”. We think US rate rises could be on the agenda by the end of 2014 or early 2015. The implications for UK rate rises should be evident. Our mantra - watch the USA and add six months - may be a little more compressed in this cycle. UK survey data … This week the February Markit/CIPS UK PMI® surveys were released. The strong upswing in the UK manufacturing sector continued in February. Output and new business continued to rise at above-trend rates. The leading index at 56.9 was up from a revised reading of 56.6 in January. In construction, the pace of expansion continued to rise sharply. The leading index scored 62.6 in February, down from a 77-month high of 64.6 in January. Still a very strong performance. In the service sector, output continues to expand strongly in the month. The headline Business Activity Index recorded 58.2 during February, little changed on January’s 58.3 and indicative of a sharp rise in activity on a monthly basis. Overall, output in construction, manufacturing and services suggest the economy continues to recover across the board at a very strong rate. The latest NIESR GDP tracker suggest growth increased by 3.5% in January. The Bank of England expects growth of over 3.5% in the first quarter. For the year as a whole, the consensus forecast is for growth of 2.7% this year. We await the details of the latest GM Chamber of Commerce survey before raising our estimates of growth this year. The GDP(O) model is signalling growth of 3% for the year as a whole. The survey data is a little more tempered, I suspect. In the UK and the USA, growth is accelerating and the job market is “tightening”. The pay round will become more difficult by the end of the year. Earnings are set to increase significantly as critical unemployment levels are breached by early 2015. Household incomes are set to improve and the recovery in spending will continue. There will be no “rebalancing”, whatever that really means. Growth up, unemployment down, inflation down and borrowing heading in the right direction. Just the trade figures will continue to disappoint. If growth hits 3% this year, disappointment could turn to shock and alarm. Then all forward rate bets will be off. So what happened to sterling? The pound closed at $1.672 from $1.675 and at 1.205 from 1.213 against the Euro. The dollar closed at 1.387 from 1.381 against the euro and 103.3 from 101.7 against the Yen. Oil Price Brent Crude closed at $108.86 from $109.02. The average price in February last year was almost $116 falling to $108 in March. Markets, moved slightly - The Dow closed at 16,458 from 16,367 and the FTSE slipped closing at 6,712 from 6,809. UK Ten year gilt yields closed at 2.81 from 2.72 and US Treasury yields closed at 2.80 from 2.67. Gold lovers worship alone with a close at $1,338. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Revisions to GDP …

The second estimates of growth in the UK and the USA were released this week. In the US growth of 3.2% in the final quarter of the year, was revised down to a more modest 2.5%. Janet Yellen, head of the Fed is prepared to dismiss recent soft economic data as possible result of the bad cold snap. For the year as a whole, US growth in 2013 was a respectable 1.9%. Most forecasters still expect US growth of 2.8% to 2.9% in 2014. In the UK, the second estimate of GDP was also released this week. Growth in 2013 was revised down to 1.8%. Oh dear, the UK is no longer the fastest growing economy in the developed world. Just as well, the balance of payments strain would have been too much. The outlook for the current year hasn’t changed overall. We still expect growth of 2.5% in the year, with the consensus forecast slightly higher around 2.7%. The right kind of growth? … But is it the right kind of growth? For the purists, probably not. For the pragmatic, what’s not to like? The service sector continued to drive expansion in the economy, with significant growth in the leisure sector along with business and financial services. Distribution, hotels and restaurant trades grew by almost 4% in the year, up by almost 5% in the final quarter. Business and financial services were up by 3% in the last quarter, up by 2.6% for the year as a whole. The service sector accounts for 80% of total output in the economy. The real driver of recovery. Good news in construction … The good news in construction continued with growth up by 4.4% in the last three months of the year. Developments in the housing sector providing foundations for recovery. Assuming we can make the bricks, growth should continue into 2014 with our forecast growth over 6% in the current year. The march of the makers … So what of the march of the makers? Growth in manufacturing output was revised down to less than 2% in the final quarter. This is particularly disappointing, since the prior year figure was a “nothing to beat number”. For the year, manufacturing output actually fell by 0.6%. Output is still almost 10% below the pre recession peak. We have to be realistic when formulating a policy for industry. We expect growth for the manufacturing sector broadly in line with total GDP this year but not much more. So what of rebalancing … Household spending last year was up by 2.5% accounting for over 60% of GDP. There is little evidence of rebalancing in the economy, either in terms of net trade or investment. Investment, accounting for 14% of total spending, actually fell slightly, despite growth of over 8% in the final three months. Was this a trend reversal, end of year? Possibly. We expect investment growth to continue into 2014 as the forward outlook clears and confidence returns to the board room. M & A activity, will assist the figures. Plus, 60% of investment is related to dwellings and commercial property. Investment in plant and machinery, the real capital stock within the economy, accounts for just 20% of total investment. With property resurgent, we expect investment growth of 8% in 2014. And what of base rates? … In the US, Janet Yellen affirmed the Fed commitment to continued tapering. QE could be eliminated by the Fall with a steady reduction of $10 billion per month. That could mean, a US rate rise could be on the agenda by the end of the year. The mantra for the UK remains watch the USA and add six months. The MPC cannot move ahead of the Fed without significant appreciation of sterling. When will UK rates rise? Martin Weale has suggested UK rates will rise in the Spring next year and could rise earlier if productivity fails to improve and inflation ticks up. Ian McCafferty a fellow MPC member suggests the rate rise may be held back because of the strength of sterling and the resultant mitigating impact on inflation. Either way, rates are set to rise, probably in 2015 but possibly after the May election. The banks are beginning to model affordability and pay back with a 5% base rate test. This may prove too severe for some years yet. The MPC would have us believe rates will be held below 2% until late 2017. David Miles in a speech to the Mile End group this week, suggests the “new normal” could include an equilibrium base rate of 2.5% to 3% over the long term. Imagine, we may never see the 4.5% base rate again! So much for 320 years of history, in which we have endured an average base rate of 4.5% to 5%. If only! New normals usually end up as the same old same olds. So what happened to sterling? The pound closed up at $1.675 from $1.664 and at 1.213 from 1.210 against the Euro. The dollar closed at 1.381 from 1.374 against the euro and 101.7 from 102.5 against the Yen. Oil Price Brent Crude closed at $109.02 from $109.67. The average price in February last year was almost $116 falling to $108 in March. Markets, moved slightly - The Dow closed at 16,367 from 16,143 and the FTSE closed at 6,809 from 6,838. UK Ten year gilt yields closed at 2.72 from 2.79 and US Treasury yields closed at 2.67 from 2.75. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  GDP growth up in the UK .. The ONS delivered the preliminary estimate of growth in the final quarter of the year this week. The UK economy grew by 2.8% year on year and 1.9% for the year as a whole. Who would believe this time last year markets were still fretting about a triple dip recession. The service sector, accounting for almost 80% of activity increased by 2.6%, construction increased by 4.5% and even the beleaguered manufacturing sector managed to push output up by 2.6%. Within the service sector, the leisure pound was once again to the fore, with strong growth in distribution, hotels and restaurants up by 4.5%. Business services increased by over 3%. We expect growth to be revised up to 2% for 2013 at some stage. For the moment we stick with our forecast of growth in 2014 and 2015 of 2.5% and 2.7% respectively. Our GDP(O) model is still performing well. The dataset has been updated and is available on the Publications page, along with our latest review of world trade. For economists, it doesn’t get more exciting. The release of the preliminary estimate is comparable to the release of a first draft of a Harry Potter chapter. What happened to the Weasleys, Gilderoy and Malfoy? Has Hagrid shaved off his beard as an end of year bet? Has Dumbledore lost weight. Has Voldemort renounced the devil and all his works? So what happened to Hermione and Harry? Can water supply and sewage really have grown by 8% in the final three months of the year? All is revealed to muggles and analysts alike by Joe Grice Chief Economist of the Office for National Statistics. In a high profile press conference, analagous to the lottery or some talent show, Joe reveals all... and the number is 1.9%. Excellent, thanks Joe. Data revisions are always interesting. But imagine if the next chapter of Rowling release revealed, the philosopher’s stone has been lost, the Chamber of Secrets has been opened to the public, the prisoner of Azkaban has been recaptured and the goblet of fire turns out to be a flaming glass of sambuca. It really can be so dramatic. After all the double dip disappeared. One day we may discover there was no recession in 2008 after all. Can’t wait for the next chapter in the GDP chronicles on the 26th February. So what happened to consumer spending and what of investment? Still stuck in the deathly hallows no doubt. US GDP also increased by 2.7% in the final quarter ... Over in the US, the Bureau of Economic Analysis announced growth of 2.7% in the final quarter and 1.9% for the year as a whole. The UK and the USA are neck an neck in the race to be the fastest growing economies in the Western World. Makes you wonder why the Fed were spending $85 million each month on treasuries and mortgage debt. No wonder the decision was made to taper further and reduce the spend to $65 billion with immediate effect. It is said that if a butterfly flaps its wings in Nicaragua, it can cause a hurricane in New York. I always found that difficult to be believe. But then who would have thought gay marriage could cause such flooding in Somerset according to UKIP. Even so, Bernanke flapping his tapering wings in Washington caused chaos in capital markets across the world. The tapering announcement led to falls in international stock markets, capital flight from developing economies and exchange rates rattling in India, Turkey and Argentina. Turkey hiked rates to over 10% to persuade the dollars to stick around. In Buenos Aires, they have long since departed. So what happened to sterling? Markets were disturbed by the decision on tapering, once again undermining stock market strength in the USA and destabilizing international capital flows across developing economies. Nevertheless, the CBOE Vix volatility index closed relatively unchanged over the week at 18.4. The pound closed at $1.6433 from $1.6481 against the dollar and 1.2184 from 1.2041 against the Euro. The dollar closing at 1.3487 from 1.3681 against the euro and 101.96 from 102.34 against the Yen. Oil Price Brent Crude closed at $106.40 from $107.88. The average price in January last year was almost $113, no real threat to inflation from crude oil prices Markets, moved down - The Dow closed at 15,698 from 15,879 and the FTSE closed at 6,5210 from 6,663. 7,000 on the FTSE no longer such a soft call for the near term. UK Ten year gilt yields closed at 2.72 from 2.78 and US Treasury yields closed at 2.65 from 2.72. Yields will test the 3% level as tapering accelerates into 2014 but for this week, once again, the flight to quality led the market. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.   Employment surge will force rethink on forward guidance …

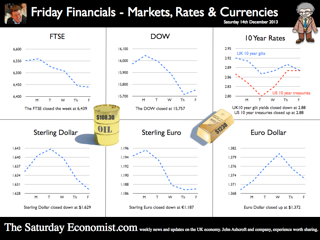

The governor went to Davos this week and also appeared on the Paxman Show. He was asked about unemployment, forward guidance and Bitcoins! Excellent. Unemployment Unemployment fell to 7.1% in the three months to November according to the latest data from the ONS. Over 30 million were in employment up by 280,000 on the prior three months. Good news for the economy and a measure of the strong recovery in the UK, particularly in the second half of the year. The claimant count measure fell by 24,000 to a rate of 3.7%. The unemployed (claimant count) will fall below the one million mark by the end of 2014 based on our current forecasts. This would be in with levels last seen in September of 2008. No need then to worry about household incomes, earnings will begin to recover significantly as the job market tightens through the year. Forward Guidance So what of forward guidance? “Mark Carney has torn up his original low interest rate policy after completely misjudging the speed at which unemployment would fall” according to Phillip Aldrick writing in The Times today. Well not really. It is true the Bank of England model assumed the 7% hurdle rate would be triggered in 2015 rather then by the end of 2013! Nevertheless, the overall parameters of forward guidance remain in tact. The major concern of central bankers is conditioned by the experience of The Great Depression and the Lost Decade. Monetary policy will remain accommodating until the recovery and “escape velocity” from recession is secured. Even then, rates will rise slowly and gradually. It will be some years before a return to equilibrium base rates of 4.5% is achieved, the additional guideline. In the Inflation Report due next month, the bank will consider a range of options to update Forward Guidance. The simplest solution, an update to the unemployment hurdle rate from 7% to 6.5%. The challenge of a more complex hybrid may prove irresistible. As for escape velocity, tapering in the US is expected to accelerate. There seems little justification, if indeed there ever was, to continue to spend Fed dollars on US Treasuries and mortgage debt. 3% growth in the USA economy appears possible this year. That’s a faster rate than in the years leading up to the collapse in 2008. Borrowing Figures The UK Government borrowing figures were released this week. The government is on track to reduce the level of borrowing to between £105 billion and £110 billion this year. Receipts are rising faster than spending and the overall level of borrowing in the first nine months of the year is down by over £5 billion. Inflation down, borrowing down, unemployment down, earnings will begin to rise later this year. The platform for the election is well set. Just the trade figures alone will continue to disappoint as problems in Europe persist. So what happened to sterling? Markets were disturbed by the possibility of more tapering, undermining stock market strength in the USA and destabilizing international capital flows across developing economies. Poor readings from manufacturing data in China and Japan, plus problems with the Argentinian peso created the “perfect storm” for markets at the end of the week. The CBOE Vix volatility index shot up from 13.8 to 18.14 at close. Some way off the 55 level recorded in the depths of despair in 2010 but a measure of late volatility nevertheless. The pound closed at $1.6481 from $1.6422 against the dollar and 1.2041 from 1.2127 against the Euro. The dollar closing at 1.3681 from 1.3538 against the euro and 102.34 104.23 against the Yen. Oil Price Brent Crude closed at $107.88 from $106.48. The average price in January last year was almost $113, so no real threat to inflation from crude oil prices Markets, moved down - The Dow closed at 15,879 from 16,458 and the FTSE closed at 6,663 from 6,829. 7,000 on the FTSE a soft call for the near term, requiring a little more work in progress. UK Ten year gilt yields closed at 2.78 from 2.84 and US Treasury yields closed at 2.72 from 2.82. Yields will test the 3% level as tapering accelerates into 2014 but for this week, the flight to quality led the market. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  “If inflation is the genie, deflation is the ogre that must be fought decisively...” Christine Lagarde head of the IMF was speaking to the National Press Club in Washington this week. With inflation below central bank targets in Japan, USA and Europe, the IMF believe the rising risks of deflation could prove disastrous for the world recovery. Western leaders, haunted by fears of the American Great Depression and Japan’s Lost Decade, are fearful of premature monetary tightening which could threaten the nascent recovery. In folklore, a genie is a supernatural creature who does the bidding once summoned. This may not have been the intentioned meaning by the boss of the IMF but Mark Carney Governor of the Bank of England, could be forgiven the interpretation. This week, the inflation figures for December were released by the ONS. CPI inflation increased by just 2%. For the first time in over four years, the genie returned to target, as would an obedient creature, undertaking the bidding of the new Governor of the Bank of England. The genie is working hard to obey. It has taken some time to get the message into the bottle and the genie back on message! Mission accomplished? With such success, it would be churlish to point out that in the same month, RPI increased from 2.6% to 2.7%, goods inflation actually went up and service sector inflation closed the year at 2.4%. For the moment the wild ride of the last four years has come to a close. As Christine Lagarde stated, “Optimism is in the air, the deep freeze is behind us and the horizon is much brighter.” In further good news, UK manufacturing prices increased by just 1% in December and input costs actually fell by just over 1%. Import prices of metals, parts and equipment fell, reflecting higher sterling values and lower world prices. For the moment, the inflation outlook for 2014 appears benign. Deflation is the ogre ... So what of ogres and deflation. Ogres are monsters in legends and fairy tales that eat humans and are particularly cruel, brutish or hideous. In the UK fears of deflation are not evident. We still expect inflation to hover slightly above target through the year. The ogre of deflation will be banished within the Kingdom. Particularly with earnings on the rise and a Chancellor of the Exchequer, as the handsome prince, up for re election, pledging an increase in the minimum wage to £7 an hour over the next couple of years. Inflation has fallen to target much faster than we had envisaged. The good news - as earnings rise, the boost to real incomes will lead to a sustained level of growth in consumer expenditure and retail sales. Higher but not quite as high as the latest UK data might suggest perhaps! Retail Sales the nymph spirit ... This week, the ONS released the retail sales figures for December. Sales volumes increased by 5.3% and values increased by 6.1% compared to December last year. Despite the fears of the major retailers, the consumer hit the high street with great gusto in the run up to Christmas allegedly. Internet sales, increased by 11.8% and small stores, experienced higher growth with sales increasing by just over 8%. Can retail sales have been so strong in December? Contractions in volume sales amongst food stores and petrols stations adds to the confused picture in the month. According to the ONS, in the three months prior to December, retail sales volumes averaged just 2%. So much for saving for Christmas. The surge in activity in December appears rather high and slightly at odds to the anecdotal evidence from retailers themselves. The BRC, British Retail Consortium suggests sales increased by just 1.8% in December as footfall actually fell. The BDO high street tracker reported sales down in the pre Christmas week with a recovery to 3.5% growth in the final week of the year. Debenhams, M & S, Morrisons and Sainsburys struggled in the Christmas period. Argos, Dixons, Halfords, Primark, Lidl and Ocado amongst the winners in the multi channel race. The 5% growth in volumes reported by the ONS appears to be a high call. So much for lies, damned lies and seasonal adjustment. Shrek shacking up with the Sleeping Beauty ... Ogres returned to the High Street this week as Sports Direct revealed a near 5% stake in Debenhams. Imagine Shrek shacking up with Sleeping Beauty, shudders must have swept around the Debenhams board room. The subsequent put and call option by Sports Direct, just added more confusion to the retail horizon. So what happened to sterling? The pound closed at £1.6422 against the dollar and 1.2127 against the Euro. The dollar closing at 1.3538 against the euro and 104.23 against the Yen. Oil Price Brent Crude closed at $106.48. The average price in January last year was almost $113, so no real threat to inflation from crude oil prices Markets, moved higher. The Dow closed at 16,458 and the FTSE closed at 6,829. 7,000 on the FTSE a soft call for the near term. UK Ten year gilt yields closed at 2.84 and US Treasury yields closed at 2.82. Yields will test the 3% level as tapering accelerates into 2014. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research and our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

The good news for policy makers continued this week as inflation and unemployment continued to head in the right direction. The latest revisions to the National Accounts suggest the economy will grow by 2% this year. Inflation CPI ... falling Inflation CPI basis fell to 2.1% in November down from 2.2% in October. Manufacturing output prices increased by less than 1% in the month, unchanged from the prior period. Input costs for manufacturers actually fell by 1% as world commodity prices including metals and oil remained subdued. Overall the inflation outlook is benign with inflationary pressures diminishing. It will take some time for world demand to impact on price levels as long as the recovery in Europe remains protracted. We expect the international inflation outlook to look pretty soft over the next twelve months. Labour Costs ... set to rise On the other hand we expect a reversal in the trend in domestic labour costs by the end of next year. The claimant count fell by 37,000 in November to a level of 1.269 million, a rate of 3.8%. The overall number of claimants, over the past year, has fallen by 300,000 down from a rate of 4.6% in November 2012. 120,000 have found work over the past three months. At the current rate of jobs growth, the claimant count rate will fall to around 2.5%, within twelve to fifteen months. This is a pre recession rate, consistent with significant growth in rates of pay and remuneration. As it is, the rate of private sector earnings increased by almost 1.5% in October. The widely reported “whole economy rate” increased by just under 1% but the warning signs are there for policy makers - domestic inflationary pressures and labour costs will be back on the MPC agenda by the end of 2014. As unemployment falls ... The wider Labour Force Survey Data confirmed the unemployment level fell to 2.388 million in October and a rate of 7.4%. This is a fall of 120,000 over the past year as the overall number of people in employment increased by almost 500,000. The 7% hurdle rate outlined in Forward Guidance could be within reach within twelve months as the rate of economic growth accelerates into the final quarter of 2013 and into next. Interest rates are set to rise, probably after the 2015 election. Bank of England MPC Minutes ... The minutes of the Bank of England Monetary Policy Committee were released this week, explaining why base rates were not increased in the December meeting. The domestic recovery was robust with inflationary pressure diminishing it was said. The GDP figures had confirmed the rapid pick up in consumption growth. Strong contribution from stock building had been offset by a large drag from net trade. The overall divergence between domestic demand and net trade had been larger than expected. Any significant narrowing of the current account deficit in the near term seemed unlikely! Rebalancing ? Does this mean the MPC had got the message about the rebalancing agenda? Sadly not. The minutes went on to claim that a sustained recovery would require some rebalancing from domestic to external demand! Some hope, the UK is set for a classic consumption rally with domestic demand growth of significant proportions. Fears about the appreciation of sterling are misguided. Higher sterling will alleviate inflationary pressures and de facto improve margins and competitiveness of exports. For exporters, demand (not price) conditions are dominant. The sluggish recovery in Europe will be the real obstacle to export growth over the next twelve months. And what of Investment ... Better news for investment however. The minutes claimed that beyond the near term, it seemed likely that a pick up in business investment spending would be necessary, Business and Dwellings investment had been weaker than expected to date. Weaker than expected in the Bank of England model, perhaps. The good news is that, we expect a strong rally in investment spending in 2014 as capital expenditure projects are brought back to the board room on the back of stronger domestic demand. Just 20% of total investment is determined by plant and machinery and our models suggest the four year capital stock has fallen to £163 billion down from an average £183 billion in the three years prior to recession. That represents a fall of 12%. Our less aggressive ten year Capital Stock Model suggests the overall level of productive investment has fallen by just 2%. No threat to the output capacity of UK PLC. The shortfall will be addressed by additional investment over the next three years to restore capacity equilibrium. Investment in transport equipment is set to rally on the back of a a 10% increase in commercial vehicle sales this year. Intangibles “investment” is set to rise on the back of a healthier M & A and corporate finance market in 2014. Together transport equipment and intangible investments account for a further 20% of total investment. Why has investment been subdued ... ? Why has investment been subdued post recession? Well in general businesses will invest in response to rising demand not a fall in the cost of capital. More specifically, 60% of investment identified in the national accounts is linked to property, either dwellings or commercial real estate. No policy maker should be surprised by the lag in investment intentions in this sector. Significant price collapse has left almost half the banked commercial real estate under water on a conventional 65% LTV (loan to value) test. A significant recovery in prices is required to restore equilibrium in the commercial real estate sector. The recovery in property and real estate may be a little more protracted, than “other investment classes”. Nevertheless we expect strong investment growth in 2014 and 2015 with investment in “dwellings” staging a marked recovery. So what of the revisions to the National Accounts? The latest revisions to the National Accounts confirm the economy grew by 2% year on year in Q3. We now expect the economy to grow by 2% for the year as a whole and by 2.5% in 2014 rising to 2.7% in the following year. And what of tapering? The Fed announced the beginning of tapering with a reduction in the rate of asset purchases by $10 billion from January 2014. What is that all about? The Fed said, “The Committee's sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee's dual mandate.” Oh dear? The link between longer term rates and growth has never been fully explained as neither has the linkage between domestic asset price inflation and international deflationary pressures. Nevertheless, it is time to buckle up, we are leaving Planet ZIRP - This week, the US growth rate was revised up to 2% year on year in Q3, Fed rates will also be on the rise in 2015. What happened to sterling? The pound closed at £1.6351 from £1.6294. Against the Euro, Sterling closed at €1.1950 from €1.1856. The dollar moved up against the yen closing at ¥104. from ¥103.6 and closing at 1.3678 from 1.3740 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant overhead resistance. Oil Price Brent Crude closed at $111.58 from $108.53. The average price in December last year was almost $110, so no real threat to inflation. Markets, US moved higher - The Dow closed at 16,275 from 15,755. The FTSE closed at 6,606 from 6,434. 7,000. UK Ten year gilt yields closed at 2.94 from 2.90 US Treasury yields closed at 2.89 from 2.87. Yields will test the 3% level as tapering accelerates. Gold closed at $1,207 from $1,239. That’s all for this week, and for this year. No Sunday Times and Croissants tomorrow or for the next few weeks. The professor and his team are away for a short break. Have a great Christmas of Holiday Break and have a Happy New Year. Join the mailing list for The Saturday Economist or forward to a friend John © 2013 The Saturday Economist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

Economics news – the spirit of Christmas present is a cheerful spirit ... The spirit of Christmas Past - should not be forgotten. The spirit of Christmas Present - is a cheerful spirit. The spirit of Christmas Yet to Come suggests that it is unlikely that equilibrium interest rates will return to historically normal levels any time soon”. Excellent. Don’t you just love a central banker with a Christmas message. Governor Carney was speaking in New York this week at the Economic Club of New York. The Governor is anxious to secure the message, interest rates will not rise any time soon. The recovery will not be put at risk. The UK will achieve escape velocity from a liquidity trap, avoiding secular stagnation in the process. Forward guidance is the new policy mantra, secular stagnation the new spectre on the blog. The UK is set for recovery, despite the prophets of gloom on either side of the Atlantic. Forward guidance is integral to the central bankers response to the recession and setback. FG reduces uncertainty, providing reassurance that monetary policy will not be tightened before the recovery is sufficiently established. Businesses will have the confidence to invest. Households will have the confidence to spend. A liquidity trap is avoided. A liquidity trap occurs when the short-term nominal interest rate hits the zero lower bound. Typically in a liquidity trap, inflation is low, the equilibrium real interest rate is negative, creating a persistent inability to match aggregate demand and supply. Businesses won’t invest and consumers are reluctant to spend, aggregate demand continues to fall and a deflationary spiral develops. Fiscal constraints ensure Government spending cannot bridge the output gap. In the UK, the financial crisis pushed the equilibrium real interest rate to the lower bound. With nominal interest rates stuck at zero, and inflation low, monetary policy was unable to push actual real rates to a level low enough to generate growth allegedly. “Pushing on a string, is no way to wag the dog”. I think Keynes said that. Hence the emergence of QE on Planet ZIRP. Allegedly, a way to stimulate liquidity AND activity. In reality, a great way to undermine the gilt curve and returns to savers and investors in the process. So what of secular stagnation? Larry Summers had recently raised the spectre of secular stagnation at the IMF meeting in November in honour of Stanley Fischer, guru of monetary theory at MIT. Secular stagnation, a concept first developed by Alvin Hansen in the 1920s suggested the “new normal” in the USA (post depression) was of lower growth, primarily a result of lower population growth and technological exhaustion. No new things to boost productivity, that sort of thing. Larry Summers, resurrected the term, suggesting the short term real interest rate consistent with full employment may have fallen to -2% -3% in the middle of the last decade. “The natural and equilibrium interest rates may have fallen significantly below zero”. “We may have to think about how we manage an economy in which the zero nominal interest rate is a chronic and systemic inhibitor of economic activity holding our economies back below their long run potential.” he said. In theory, the Fed funds rate can be kept at ZIRP forever but it is much harder to do “extraordinary additional stuff” forever” either in the form of QE, or government deficit funding perhaps. This said Summers, is “my” lesson from this crisis which the world has “under internalised”. Actually Summers went on to say “Now this may all be madness and I may not have this right at all”. Mmm. Stuck on Planet ZIRP, QE was introduced, the effect of which, was to ensure we were marooned on the planet for longer. ZIRP creates of itself a problem which is compounded by QE. In the UK, QE has lost intellectual credibility and momentum but in the USA the persistent purchase of Treasuries and Mortgages (CMBS) continues, achieving no more for Uncle Sam, than a monthly dispensation into a NASDAQ tracker fund. It really is time to begin tapering in the US, end QE and return the equilibrium rate of interest to a natural rate. A natural rate for gilts and treasuries, which reflects an inflation hedge and a real rate of return to risk. In his speech, Summers said, “we have learned one thing, finance cannot be left to the financiers”. Perhaps but then I have always felt much the same about monetary economics. We should begin to think how we can manage an economy in which the academics are confined to campus and not allowed near policy levers. The concept of a negative equilibrium interest rate, which may have fallen to -3% pre recession is as incomprehensible, as life on Planet ZIRP without oxygen. The escape from ZIRP and the beginning of recovery can only be accelerated by an end to QE. Let the free markets free and end QE - the cry. It is time to suggest “Schools out for Summers” and the MIT class of 14462. The US is set to grow by over 2.5% next year or has no one noticed. Back in the UK Back in the UK, as expected the march of the makers picked up the pace in October. Manufacturing growth year on year increased to 2.7% in the month. Construction output grew at over 5% in the latest data for October. The trade figures on the other hand continued to disappoint. The UK's deficit on trade in goods and services was estimated to have been £2.6 billion in October 2013, unchanged from September. The deficit of £9.7 billion on goods, partly offset by an estimated surplus of £7.1 billion on services. Yes, the march of the makers is picking up pace, momentum is “building”, investment plans will be brought back to the board room, just the trade figures alone will continue to disappoint, as the UK recovery gains pace. What happened to sterling? The pound closed at £1.6294 from £1.6346. Against the Euro, Sterling closed at €1.1856 from €1.1922. The dollar moved down up the yen closing at ¥103.2 from ¥102.8 and closing at 1.3740 from 1.3700 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant overhead resistance. Oil Price Brent Crude closed at $108.83 from $111.61. The average price in December last year was almost $110, so no threat to inflation. Markets, US moved lower - The Dow closed at 15,755 from 16,020. The FTSE closed at 6,434 from 6,552. 7,000 FTSE now a tough call before Christmas. The markets still nervous until tapering finally begins. UK Ten year gilt yields closed at 2.90 from 2.91 US Treasury yields closed at 2.87 from 2.86. Yields will test the 3% level over the coming months but this will await the New Year. Gold closed at $1,239 from $1,231. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or why not forward to a colleague or friend? © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

The release of the second estimate of GDP in the 3rd quarter brought few surprises. Growth was confirmed at 1.7% year on year following growth of 1.4% in the second quarter.

Service sector output continues to drive the recovery with particularly strong growth in the leisure sector. Construction output increased by 4% with manufacturing growth relatively flat in the latest three month period. In current value spending terms the economy grew by 3.8% as incomes of employees and businesses continued to show strong growth. Expenditure within the economy was driven by household spending up by 2.4% in real terms plus a build up in inventories. Government spending was up by just 1.1%, investment fell slightly and the trade figures continue to disappoint. Exports fell and imports increased as UK domestic demand exceeded the rate of growth in Europe and the USA. So what does this all mean? We expect strong growth to continue into the final quarter with overall growth around 2.4% bringing the year on year growth rate to 1.3%. We still think the economy is on track for growth of around 2.4% in 2014. Check out our latest publication “Modeling GDP(O)”. We release the forecasts of the ten key sectors and sub sectors in the UK economy over the next two years. Should we too worried by the lack of investment? Not really. At this stage in the cycle we would expect investment to be weak. Plant and machinery accounts for just 20%, of total investment. Spending on commercial real estate will continue to be subdued for some time yet as the overhang continues. We expect strong growth in productive capacity in the final quarter of the year and into next year. The four year capital stock model is down by just 15% from the peaks of 2008. No need to worry about “lost output” for the years ahead, trend rate of growth can be recovered and maintained. Investment will receive a significant boost in the final three months of the year and into next. Our UK investment model will be released next week. Prospects for the UK look good, but without a strong recovery in Europe and sustained growth in the USA, the trade figures will continue to be a net drain on overall performance. This should be no surprise to regular readers! The trade deficit in goods will increase largely (but not entirely) offset by a strong performance in service sector exports. Is this the wrong kind of growth? The UK economy has been dependent on domestic consumption since our records began. Growth based on investment and exports a policy dreamboat. There will be no rebalancing of the economy just more of the same to come. Bank moves on mortage lending Which is perhaps why the Bank of England modified the terms of FLS away from mortgage lending towards business loans. The old lady is no fan of the help to buy votes scheme. The Governor has made it clear the Bank of England will move to prevent another housing boom. The policy response includes several options this time around including post code selective spread and capital provisions to curb excessive movements in house prices if necessary. What happened to sterling? The pound closed up at £1.6360 from £1.6215. Against the Euro, Sterling closed at €1.2045 from €1.1966. The dollar moved down up the yen closing at ¥102.4 from ¥101.3 and closing at 1.3582 from 1.3555 against the Euro. Sterling is on a rally which has led to a break out above £1.60, pushing through resistance at €1.20 euro basis. Oil Price Brent Crude closed at $109.65 from $111.05. The average price in November last year was almost $110. The average price just $106 this year. Markets, US pushed higher - The Dow closed at 16,086 up from 16,065. The FTSE closed at 6,650 from 6,674. 7,000 FTSE still the call before Christmas. UK Ten year gilt yields closed at 2.78 from 2.79 US Treasury yields closed at 2.75 from 2.74. Yields will test the 3% level over the coming months but this may await the New Year. Gold closed at $1,252 from $1,244. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist, #TheSaturdayEconomist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

May 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |